A new state-level analysis shows that retrofitting existing facilities with carbon capture and deploying carbon dioxide (CO2) transport infrastructure can deliver jobs and economic benefits while reducing emissions across industries. The Great Plains Institute recently commissioned Rhodium Group to conduct an independent, state-by-state analysis exploring the economic benefits of carbon capture deployment opportunities in the US. GPI identified the facilities examined in this analysis as carbon capture retrofit projects with near- to medium-term feasibility.

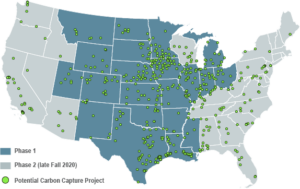

The analysis is part of a two-phase project, with the first phase focused on the Midwest, Gulf Coast, Rockies, and Northern Plains. The next phase of results on the remaining states in the lower 48 is set to publish in December 2020. The first phase’s data is also incorporated in 21 state-level fact sheets on the economic and jobs potential of carbon capture.

Key takeaways:

- There are significant state-level economic opportunities and emissions reduction potential for carbon capture deployment on existing industrial and electric power facilities in the Phase I region.

- Carbon capture can help states play to their existing and unique strengths on their paths to decarbonization.

- Carbon capture is an “off-the-shelf” technology that can be applied across key sectors to achieve a net-zero carbon economy while preserving and creating high-wage jobs.

You can view a recording of a recent webinar with Rhodium Group featuring the details of the jobs and economic impact analysis at the end of this post. The webinar was a presentation to the Regional Carbon Capture Deployment Initiative, which is staffed by GPI.

Analysis provides state-level data on the economic potential of carbon capture deployment and associated infrastructure deployment

On our recent webinar, GPI Vice President Brad Crabtree shared that this analysis is a response to state officials and stakeholders across the country asking for a “better understanding of the jobs and economic impacts of how carbon capture would benefit their states and communities in practical, tangible ways, going beyond just obvious emission reduction benefits.”

This phase of the analysis found that the states in the study region have an immense opportunity to create jobs and reduce emissions in the industrial sector, as well as at coal and gas power plants, by retrofitting existing facilities with carbon capture equipment and building transport infrastructure necessary to deliver CO2 to permanent storage locations.

POTENTIAL CARBON CAPTURE RETROFITS IN THE PHASE I STUDY REGION

Key findings from the Phase I analysis:

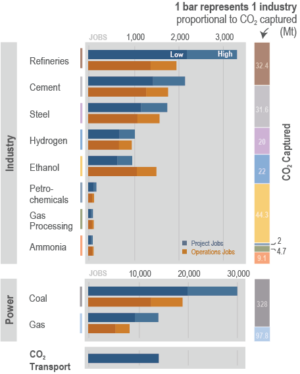

- The Phase I region’s 309 industrial facilities can create an annual average of up to 9,815 project jobs and 8,370 ongoing operations jobs while capturing 166.1 million metric tons of CO2 per year.

- The region also has 116 power plants that, combined, can create an annual average of up to 44,380 project jobs and 27,450 ongoing operations jobs while capturing 425.8 million metric tons of CO2 per year.

- The development of CO2 transport infrastructure would create an annual average of 14,130 project jobs in the Phase I region.

- The retrofit of equipment at these facilities would capture 592 million metric tons of CO2 per year.

- Along with the development of CO2 transport infrastructure, this would generate up to $212.93 billion in private investment.

The analysis considers opportunities at existing plants across all industrial subsectors and the electric power sector. The direct economic benefits considered include private sector investment and employment opportunities associated with the construction and operation of carbon capture equipment. The results show how individual states can play to their existing and unique strengths on their separate paths to decarbonization.

PHASE I STUDY REGION: ANNUAL PROJECT AND OPERATIONS JOBS

The analysis uses facilities within the Phase I region that were identified as near- and medium-term candidates for carbon capture retrofit in the recently published white paper, Transport Infrastructure for Carbon Capture and Storage: Regional Infrastructure for Midcentury Decarbonization, and translates project investment and operation costs into employment potential on a state-by-state basis.

A new series of state fact sheets highlighting the potential jobs creation and economic impact of carbon capture deployment is now available on the Carbon Capture Ready website. Forthcoming analysis will explore the economic impacts of carbon capture in the rest of the US lower 48, as well as expanded deployment of carbon capture past 2035 to meet midcentury decarbonization targets nationwide.

Carbon capture an essential part of the shift to a net-zero carbon economy

Globally, more than 30 carbon capture projects have been announced since 2017, and financial project investment has nearly doubled. According to the Global CCS Institute, meeting the Paris climate targets will require building between 70 and 100 carbon capture facilities per year for the next 30 years.

There are more than two dozen carbon capture projects on the drawing board in the US, including one project securing financing, two companies that have completed front-end engineering and design (FEED) studies for several projects, 15 projects that are conducting FEED studies, and five projects in pre-FEED status. If these projects reach commercial operation, it will represent roughly a tripling of commercial carbon capture projects in the US and an essential early down payment on long-term deployment goals.

The way we produce and consume energy is changing. As consumers, companies, and countries move toward a net-zero carbon economy, carbon capture is an “off-the-shelf” decarbonization technology that can be utilized across multiple sectors to achieve essential emissions reductions, while preserving and creating quality jobs and providing significant economic benefits.

Watch the recent webinar with Rhodium Group featuring the details of the jobs and economic impact analysis.

This blog was originally published by Great Plains Institute.